What is tariff engineering?

The legal foundation

The Supreme Court established tariff engineering in Merritt v. Welsh, 104 US 694 (1882). The Court held that importers may lawfully arrange their merchandise to fall within the lowest applicable tariff classification, as long as the classification is accurate at the moment the goods enter US commerce. The principle has been reaffirmed in modern decisions including Heartland By-Products v. United States (Fed. Cir. 2001).

The key constraint: the product must actually be what the lower classification describes. You cannot "engineer" by simply labeling — the physical characteristics must match the classification criteria.

Classic examples

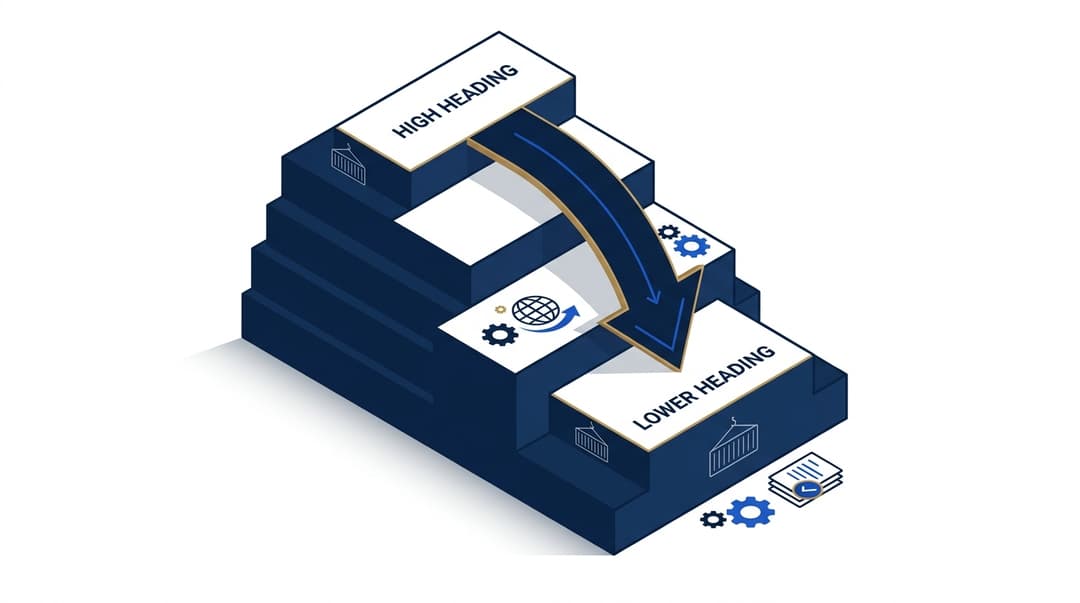

Footwear with foxing bands — The HTSUS distinguishes athletic from non-athletic footwear based partly on whether the upper is secured to the sole with a foxing band. A manufacturer designing a shoe that avoids the foxing band specification moves into a lower-duty heading.

Columbia Sportswear tab — Columbia added a small internal fabric tab to women's shirts. The tab caused the shirts to classify as "other garments" at a lower rate than the plain-shirt heading. The Court of International Trade upheld the classification.

Ford Transit Connect vans — Ford imported passenger vans, then removed rear seats post-entry to convert to cargo configuration. The Federal Circuit in Ford Motor v. United States (2019) ruled against Ford because the conversion happened post-entry with clear intent to evade. This is where tariff engineering crossed into circumvention.

The Ford case is the important boundary: the product must be what it is classified as at time of entry. Post-entry reconfiguration with pre-import intent to convert is not legal tariff engineering.

Where tariff engineering is used today

- Electronics — Configuring devices to fall under 8517 (telecom apparatus) vs 8471 (computers) vs 8528 (monitors) based on primary function

- Textiles and apparel — Fabric composition, garment construction, and accessory additions that shift HTS lines

- Footwear — Upper material ratios, sole construction, foxing bands

- Food and beverage — Ingredient ratios that cross key HTS thresholds (e.g. sugar content in flavored beverages)

- Chemicals — Purity levels and blend ratios

- Vehicles — Passenger vs cargo configuration (post-Ford, done carefully)

When tariff engineering becomes fraud

The line between lawful tariff engineering and duty evasion under 19 USC 1592:

| Lawful tariff engineering | Unlawful duty evasion |

|---|---|

| Product meets the classification criteria at entry | Product is misrepresented on entry documents |

| Manufactured specifically to meet the target HTS | Post-entry modification to evade declared classification |

| Declared accurately on Form 7501 | Declared under wrong HTS to pay less duty |

| Reviewed with licensed broker | Done without classification analysis |

| Supported by lab testing and design records | Unsupported by physical evidence |

Penalties for duty evasion under 19 USC 1592(c) include penalties up to the domestic value of the goods for fraud, 2 to 4 times the duty loss for gross negligence, and the duty loss plus interest for negligence.

How it fits with the current tariff environment

Tariff engineering is a compliance play, not a refund play. It reduces future duty exposure by classifying correctly into lower-rate headings going forward. It does not retroactively refund duty already paid.

For retroactive recovery on IEEPA duties, see the IEEPA refund calculator and the the IEEPA-refund context guide. Pair the refund with a forward-looking tariff engineering review to compress exposure.

What a tariff engineering review looks like

- Product portfolio analysis — map current HTS classifications and duty paid per SKU

- Rate-sensitive SKU identification — where small classification differences produce large duty swings

- Physical characteristic review — what technical attributes drive classification

- Design modification options — what production or sourcing changes could move the HTS

- Ruling request preparation — submit prospective ruling to CBP under 19 CFR 177 for binding classification

- Implementation with licensed broker sign-off — ensure entry-level accuracy

Binding rulings are your friend

File a prospective ruling under 19 CFR 177 before implementing. A binding ruling from CBP protects you against reclassification during audit. The Customs Rulings Online Search System (CROSS) lets you research precedent before asking.

Calculate your tariff refund → /calculators/ieepa-refund

Related questions

Is first sale valuation still legal? Yes, with caveats. See first sale legal.

Can I combine tariff engineering with drawback? Yes. Engineering reduces forward duty; drawback recovers past duty on exports.

What about First Sale for export? First Sale is a valuation tool, not a classification tool. See first sale.

Not legal advice. Customs business performed by licensed customs broker partners under 19 CFR 111.

Keep reading

first-sale valuation legal compliance

Three-party transaction and CBP rulings basics.

Read more →

HTS reclassification rulings walkthrough

Binding ruling process for revised classification.

Read more →

first-sale valuation deep-dive guide

Complete guide to first-sale program design.

Read more →

IEEPA refund interplay with future-entry strategy

Why tariff engineering pairs with refund recovery.

Read more →Related questions

Find out what you’re actually owed.

Run the IEEPA refund calculator or take the 60-second qualification quiz. Estimate only — subject to CBP adjudication.