Is first sale valuation still legal?

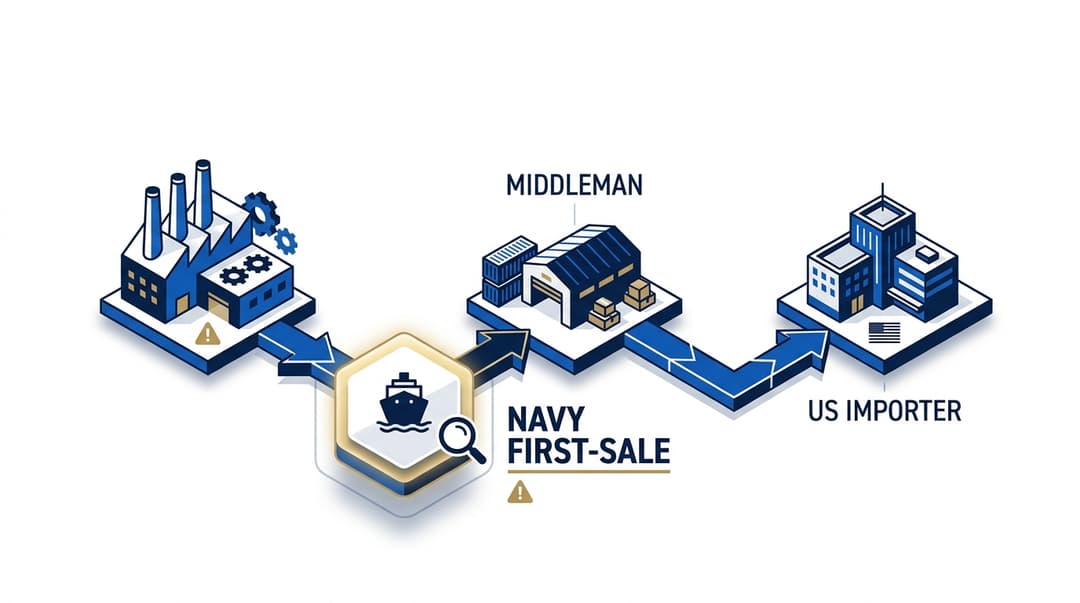

What first sale is

In a multi-tier supply chain, US import duty is normally based on the price paid by the US importer (the "last sale"). First sale lets the importer declare a lower price — the price paid in an earlier transaction in the chain — as the dutiable value, provided the transaction meets specific tests.

Example: A US importer buys shoes from a Hong Kong trading company at $20 per pair. The Hong Kong trader bought them from the Vietnamese factory at $12 per pair. Under first sale, the US importer can declare $12 as the customs value, saving duty on the $8 markup.

On $10M in annual imports at a 10 percent duty rate, first sale on a 40 percent markup can save $400,000 per year.

The Nissho Iwai three-part test

Federal Circuit in Nissho Iwai v. United States, 982 F.2d 505 (Fed. Cir. 1992) established the test. CBP codified it in Treasury Decision 96-87. All three must be true:

- Bona fide sale — There must be a genuine, arm's-length transaction between the factory and the middleman. Not a paper transaction, not an agent arrangement, not a consignment.

- Goods clearly destined for US export — At the time of the first sale, the goods must be unambiguously intended for export to the US. Evidence: purchase orders, shipping instructions, specifications.

- Arm's-length pricing — The first-sale price must reflect genuine market value, not a transfer-pricing manipulation between related parties.

Documentation required

To sustain first sale in a CBP audit under 19 CFR 163, you need:

- Three-party contract chain showing factory → middleman → US importer

- Commercial invoice from the factory to the middleman

- Commercial invoice from the middleman to the US importer

- Purchase orders showing US destination at the time of the first sale

- Transfer-pricing documentation if any parties are related

- Payment records (wire transfers, letters of credit) proving both transactions occurred

- Shipping documents showing goods moved directly or through an intermediary

Missing any one element invites denial on audit. CBP's informed compliance publication on first sale details the full documentation expectation.

What the Cassidy bill would change

The Remove Tariff Loophole Act (S. 484, Senator Bill Cassidy, reintroduced 2025) would amend 19 USC 1401a to eliminate first sale as a valuation basis. If passed, importers would be forced to declare the price paid by the US importer, increasing dutiable value across most multi-tier supply chains.

Status as of April 22, 2026: referred to Senate Finance Committee, no markup scheduled. Most trade compliance professionals expect either:

- Bill fails in committee (most likely)

- Bill passes with a sunset or transition period

- Narrower version passes that eliminates first sale only for Section 301 or sanctioned-country goods

Until it passes, first sale remains fully lawful.

Related-party pricing complications

If your factory, middleman, or importer are related parties (common ownership, officers, etc.), the arm's-length test is more demanding. CBP evaluates under 19 CFR 152.103(l) "circumstances of sale" or "test values." Transfer-pricing studies from your tax team (Section 482) are useful but not determinative — the customs value standard is separate.

First sale with current tariffs

First sale savings stack with Section 301 and remaining tariffs. On an entry subject to 25 percent Section 301 plus 2.6 percent MFN, first sale reducing the declared value from $20 to $12 saves 27.6 percent on the $8 delta — $2.21 per pair. Across high-volume supply chains, this is material.

For IEEPA refunds on past entries, first sale does not apply retroactively unless you filed with first sale originally. Going forward, combining first sale with tariff engineering (see tariff engineering) is the standard compliance playbook.

Red flags to avoid

- Invoice gap-filling — the middleman's invoice cannot just split the factory's invoice; both must reflect genuine sales

- Circular routing — goods shipped directly from factory to US while a paper middleman transaction happens elsewhere fails the "destined for US export" test

- Round-number margins — 40 percent markup on every SKU looks like transfer pricing, not market reality

- No independent documentation — if the middleman has no actual role, CBP will deny

Calculate your tariff refund → /calculators/ieepa-refund

Related questions

What is tariff engineering? See the tariff-engineering definition.

Can I combine first sale with drawback? Yes. First sale reduces dutiable value; drawback refunds on export.

Do I need a broker to use first sale? Strongly recommended under 19 CFR 111. Valuation errors trigger 19 USC 1592 penalties.

Not legal advice. Customs business performed by licensed customs broker partners under 19 CFR 111.

Keep reading

tariff-engineering basics and CBP rulings

Legal ways to lower future-entry exposure.

Read more →

first-sale valuation guide for importers

Three-party transaction structure and audit risk.

Read more →

HTS reclassification as a duty-reduction strategy

Lowering Column 1 exposure through correct classification.

Read more →

Section 232 exclusion application process

Steel and aluminum exclusion requests and outcomes.

Read more →Related questions

Find out what you’re actually owed.

Run the IEEPA refund calculator or take the 60-second qualification quiz. Estimate only — subject to CBP adjudication.